White-Label Computer Peripheral Packaging Market Size and Share Forecast Outlook 2026 to 2036

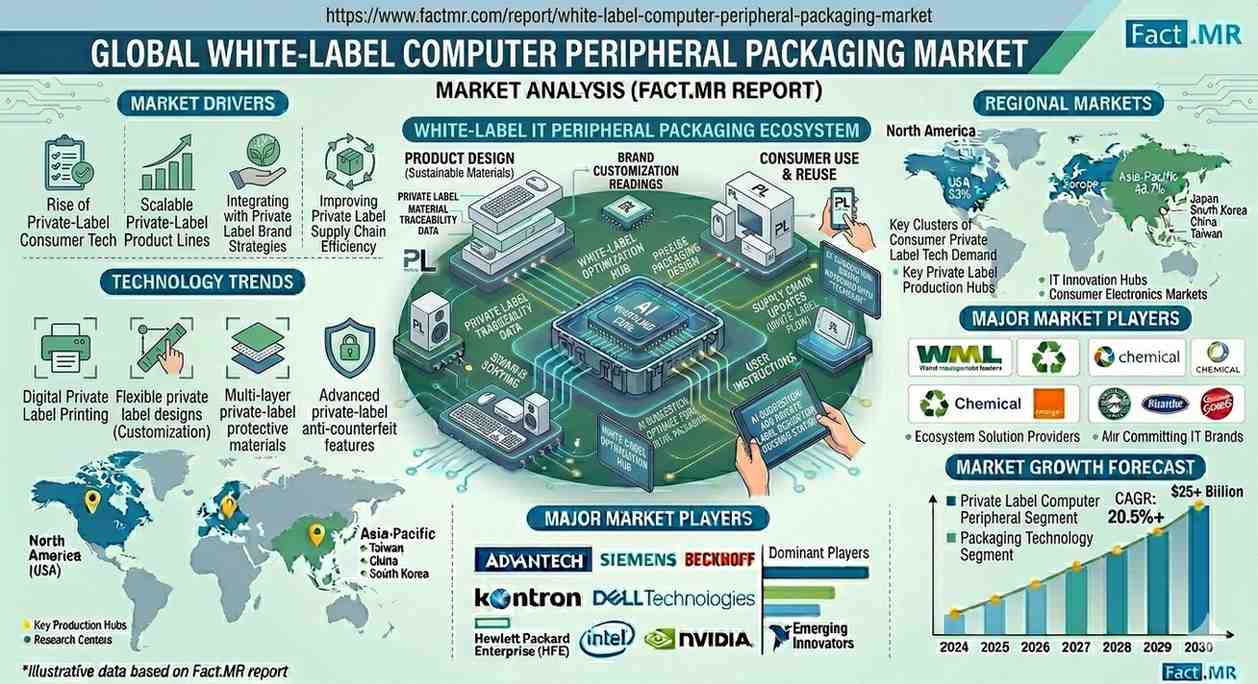

ROCKVILLE, MD, UNITED STATES, April 7, 2026 /EINPresswire.com/ — The global white-label computer peripheral packaging market is positioned for steady expansion, with a projected valuation increase from USD 535.5 million in 2026 to USD 932.2 million by 2036. This growth, representing a compound annual growth rate (CAGR) of 5.7%, highlights a fundamental shift in the electronics supply chain toward cost-efficient, neutral, and rapidly customizable packaging solutions.

As retailers, OEMs, and third-party logistics (3PL) providers aggressively expand their private-label portfolios—ranging from keyboards and mice to high-speed chargers—the demand for “brand-agnostic” yet high-quality packaging has become a strategic necessity for high-volume market penetration.

Get Access Report Sample :

https://www.factmr.com/connectus/sample?flag=S&rep_id=13926

Executive Market Summary (2026–2036)

2026 Valuation: USD 535.5 Million

2036 Projection: USD 932.2 Million

CAGR:7%

Dominant Packaging Type: Folding Cartons (48.3% Market Share)

Primary Customer Type: OEM Private Label (44.1% Market Share)

Leading Material: Paperboard (56.7% Market Share)

Strategic Segment Intelligence

Folding Cartons: The Utility Champion

Commanding nearly half the market at 48.3%, Folding Cartons are the preferred format for white-label programs. Their dominance is rooted in “artwork flexibility,” allowing manufacturers to switch branding for different retailers or distributors without altering the structural die-cuts. This modularity is essential for reducing lead times in the fast-moving peripheral sector.

OEM Private Label: Driving the Volume

The OEM Private Label segment accounts for 44.1% of the market. This reflects the “Contract Manufacturing” boom, where global factories produce standardized hardware that requires neutral, compliant packaging ready for localized branding. This segment prioritizes packaging that scales across multiple regions while adhering to international regulatory labeling standards.

Material Evolution: Paperboard Over Plastics

Paperboard holds a 56.7% share, favored for its superior printability and recyclability. While Plastics and Hybrid Structures remain relevant for high-visibility retail blister packs, the industry-wide move toward sustainability and “plastic-free” initiatives is solidifying paperboard’s position as the primary white-label substrate.

Regional Performance: India and Vietnam Lead the High-Growth Tier

Manufacturing hubs in Asia and near-shoring centers in Mexico are seeing the most aggressive adoption of white-label packaging platforms.

Country

Projected CAGR (2026-2036)

Primary Growth Driver

India

7.4%

Explosion of “D2C” (Direct-to-Consumer) and marketplace-owned brands.

Vietnam

6.8%

Massive uptick in OEM manufacturing for global private-label exports.

Indonesia

6.4%

Growth in local retail-chain brands and e-commerce fulfillment hubs.

China

5.7%

Standardized production for 3PL and cross-border fulfillment brands.

Mexico

5.3%

Regional assembly and private-label distribution for the N. American market.

USA

3.2%

Mature market focusing on rapid brand onboarding and compliance.

Competitive Landscape & Supply Chain

The competitive environment is defined by “Agile Fulfillment.” Suppliers are no longer just selling boxes; they are providing Standardized Packaging Platforms that allow for “Late-Stage Customization.”

Market Leaders: Mondi, Smurfit Kappa, and WestRock lead the paperboard segment, focusing on high-speed print lines for rapid private-label launches.

Protective Specialists: Sealed Air, Ranpak, and Berry Global provide the internal cushioning and protective mailers essential for 3PL and e-commerce fulfillment.

Integration Partners: Avery Dennison and NEFAB offer specialized labeling and transit-ready solutions that bridge the gap between OEM manufacturing and final retail delivery.

Actionable Insights for Decision-Makers

Investment Opportunities

Hybrid Fulfillment Models: Significant ROI exists in packaging that is “Retail-Ready” but “E-commerce Optimized,” allowing white-label brands to move inventory between channels without re-packaging.

Variable Print Technology: Digital printing investments allow suppliers to offer smaller “Minimum Order Quantities” (MOQs) to niche white-label startups, a high-margin growth area.

Market Risks & Challenges

Cost vs. Compliance: White-label products operate on thin margins; the primary risk is the rising cost of sustainable materials conflicting with the “low-cost” positioning of private-label goods.

Speed-to-Market: The inability of a supplier to execute rapid branding changes can lead to missed seasonal launch windows in the volatile tech sector.

Future Outlook: The “Invisible” Supply Chain

By 2036, the white-label packaging market will be characterized by Neutral-Stock Intelligence. Packaging will be produced in generic, unbranded batches and “digitally dressed” via automated labeling or high-speed inkjet systems at the point of fulfillment. This shift will drastically reduce inventory waste and allow retailers to launch “Store-Brand” peripherals in a fraction of current development cycles.

Browse Full Report –

https://www.factmr.com/report/white-label-computer-peripheral-packaging-market

To View Related Report:

Computer Aided Dispatch (CAD) Market https://www.factmr.com/report/3060/computer-aided-dispatch-cad-market

Computer Aided Engineering Market https://www.factmr.com/report/4620/computer-aided-engineering-market

Supercomputer Market https://www.factmr.com/report/supercomputer-market

Brain-Computer Interface Market https://www.factmr.com/report/brain-computer-interface-market

S. N. Jha

Fact.MR

+1 628-251-1583

email us here

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery